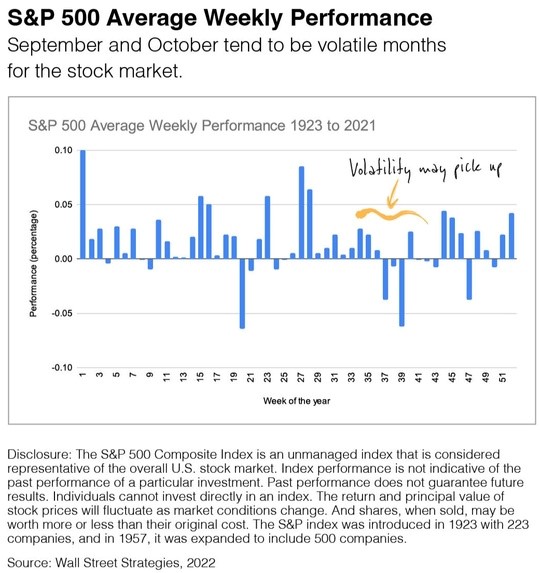

We’re entering a tricky time of year: September and October have a reputation for bringing an extra measure of market volatility.

Some of the stock market’s most challenging events have hit in September and October, and other seasonal trends can also play a part. Investopedia found that institutions start preparing for year-end distributions around this time. Plus, individuals tend to reposition their portfolios after the summer months.

This chart shows the average weekly S&P 500 performance since 1923. I’ve highlighted September and October so you can see how they compare to the rest of the year.

So what’s an investor to do? Just be prepared to roll with an uptick in volatility, and don’t let seasonal trading influence your overall strategy. For questions and concerns, feel free to reach out to info@capstoneRG.com and a Capstone Consultant will be in contact.

With half the year behind us, now is a great time to consider what the remainder of 2022 may hold. However, with inflation and economic uncertainty causing many of us to delay or cancel vacations, large purchases, and more, it can be challenging to know where to start.

Here are a few tips to help make the rest of the year as smooth as possible:

Deflate Inflation – Travel-related costs have skyrocketed, causing many to delay or cancel vacation plans. But are you overreacting to current headlines? Let’s talk if you’re wavering on a scheduled trip.

Embrace Uncertainty – If you’ve delayed a major purchase lately, you’re not alone. Economic uncertainty has caused many to rethink their expenditures. When your net worth declines, the “wealth effect” tells consumers to rein in spending. But our portfolio strategy takes into account periods of market volatility.

Practice Patience – The need to take action can push even the most seasoned investors into questionable territory. Instead, try to take a long view of the markets. Remaining patient and taking a break from watching the markets closely may help weather the storm.

Let us know if you ever want to chat about your future goals or current economic conditions. We’re always ready to help.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS), an affiliate of Kestra IS. [Capstone Retirement Group] and any other entity listed herein are not affiliated with Kestra IS or Kestra AS. Investor Disclosures: https://www.kestrafinancial.com/disclosures

“Be fearful when others are greedy and greedy when others are fearful,” according to legendary investor Warren Buffett. It’s a great quote but complex advice to follow, especially in 2022 when stock prices are down double-digits. It seems like company after company is telling shareholders it will be a challenging year. But has fearful sentiment reached an extreme? According to an April survey by the American Association of Individual Investors, nearly 60% of individual investors describe their six-month outlook for stocks as “bearish”–the highest level since March 2009. A.A.I.I. has been surveying investors since 1987, and the April bearish figure is the 10th highest in history.

The A.A.I.I. has a lot of research into what happens when sentiment gets stretched on bullish and bearish sides. But the most important research takes into account your specific goals, time horizon, and risk tolerance. Please reach out if you feel a bit queasy about today’s markets. The best medicine may be a dose of reassurance.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright FMG Suite.

One of the common threads of a mobile workforce is that many individuals who leave their job are faced with a decision about what to do with their 401(k) account.¹

Individuals have four choices with the 401(k) account they accrued at a previous employer.2

Choice 1: Leave It with Your Previous Employer

You may choose to do nothing and leave your account in your previous employer’s 401(k) plan. However, if your account balance is under a certain amount, be aware that your ex-employer may elect to distribute the funds to you.

There may be reasons to keep your 401(k) with your previous employer —such as investments that are low cost or have limited availability outside of the plan. Other reasons are to maintain certain creditor protections that are unique to qualified retirement plans, or to retain the ability to borrow from it, if the plan allows for such loans to ex-employees.3

The primary downside is that individuals can become disconnected from the old account and pay less attention to the ongoing management of its investments.

Choice 2: Transfer to Your New Employer’s 401(k) Plan

Provided your current employer’s 401(k) accepts the transfer of assets from a pre-existing 401(k), you may want to consider moving these assets to your new plan.

The primary benefits to transferring are the convenience of consolidating your assets, retaining their strong creditor protections, and keeping them accessible via the plan’s loan feature.

If the new plan has a competitive investment menu, many individuals prefer to transfer their account and make a full break with their former employer.

Choice 3: Roll Over Assets to a Traditional Individual Retirement Account (IRA)

Another choice is to roll assets over into a new or existing traditional IRA. It’s possible that a traditional IRA may provide some investment choices that may not exist in your new 401(k) plan.4

The drawback to this approach may be less creditor protection and the loss of access to these funds via a 401(k) loan feature.

Remember, don’t feel rushed into making a decision. You have time to consider your choices and may want to seek professional guidance to answer any questions you may have.

Choice 4: Cash out the account

The last choice is to simply cash out of the account. However, if you choose to cash out, you may be required to pay ordinary income tax on the balance plus a 10% early withdrawal penalty if you are under age 59½. In addition, employers may hold onto 20% of your account balance to prepay the taxes you’ll owe.

Think carefully before deciding to cash out a retirement plan. Aside from the costs of the early withdrawal penalty, there’s an additional opportunity cost in taking money out of an account that could potentially grow on a tax-deferred basis. For example, taking $10,000 out of a 401(k) instead of rolling over into an account earning an average of 8% in tax-deferred earnings could leave you $100,000 short after 30 years.5

1. In most circumstances, you must begin taking required minimum distributions from your 401(k) or other defined contribution plan in the year you turn 72. Withdrawals from your 401(k) or other defined contribution plans are taxed as ordinary income, and if taken before age 59½, may be subject to a 10% federal income tax penalty. 2. FINRA.org, 2022 3. A 401(k) loan not paid is deemed a distribution, subject to income taxes and a 10% tax penalty if the account owner is under 59½. If the account owner switches jobs or gets laid off, any outstanding 401(k) loan balance becomes due by the time the person files his or her federal tax return. 4. In most circumstances, once you reach age 72, you must begin taking required minimum distributions from a Traditional Individual Retirement Account (IRA). Withdrawals from Traditional IRAs are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty. You may continue to contribute to a Traditional IRA past age 70½ as long as you meet the earned-income requirement. 5. This is a hypothetical example used for illustrative purposes only. It is not representative of any specific investment or combination of investments.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright FMG Suite.

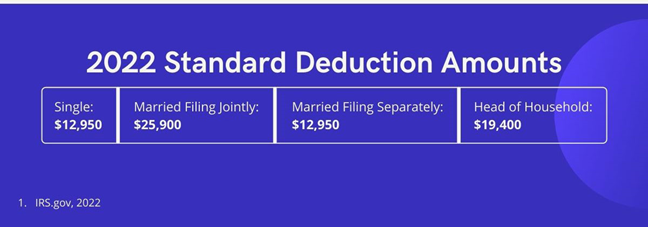

Every year, the IRS evaluates and typically adjusts certain tax provisions to account for inflation. Below is the IRS’s latest adjustments for the 2022 tax year – including tax brackets and standard deductions.

This material is for informational purposes only and is not a replacement for real-life advice, so make sure to consult your tax, legal, and accounting professionals before modifying your tax strategy.

When our parents retired, living to 75 amounted to a nice long life, and Social Security was often supplemented by a pension. The Social Security Administration (SSA) estimates that today’s average 65-year-old woman will live to age 86½. Given these projections, it appears that a retirement of 20 years or longer might be in your future.1

Are you prepared for a 20-year retirement?

How about a 30-year or even 40-year retirement? Don’t laugh; it could happen. The Society of Actuaries predicts that an average healthy woman that reaches age 65 has a 44% chance of living past 90, and a 22% chance of living to be older than 95.2

Start with good questions.

How can you draw retirement income from what you’ve saved? How might you create other income streams to complement Social Security? And what are some ways you can protect your retirement savings and other financial assets?

Enlist a financial professional.

The right person can give you some good ideas, especially one who understands the challenges women face in saving for retirement. These may include income inequality or time out of the workforce due to childcare or eldercare. It could also mean helping you maintain financial equilibrium in the wake of divorce or the death of a spouse.

Invest strategically.

If you are in your fifties, you have less time to make back any big investment losses than you once did. So, protecting what you have may be a priority. At the same time, the possibility of a retirement lasting up to 30 or 40 years will require a good understanding of your risk tolerance and overall goals.

Consider extended care coverage.

Women have longer average life expectancies than men and may require significant periods of eldercare. Medicare is no substitute for extended care insurance; it only covers a few weeks of nursing home care, and that may only apply under special circumstances. Extended care coverage can provide financial relief if the need arises.3

Claim Social Security benefits carefully.

If your career and health permit, delaying Social Security can be a wise move. If you wait until full retirement age to claim your benefits, you could receive larger Social Security payments as a result. For every year you wait to claim Social Security past your full retirement age up until age 70, your monthly payments get about 8% larger.4

Retire with a strategy.

As you face retirement, a financial professional who understands your unique goals can help you design an approach that can serve you well for years to come.

1. SSA.gov, 2021 2. LongevityIllustrator.org, 2021. Life expectancy estimates assume average health, non-smoker, and a retirement age of 65. 3. Medicare.gov, 2021 4. SSA.gov, 2021

The average household with revolving credit card debt had a balance of $6,006 in 2021. For the average household carrying credit card debt in 2021, this equated to an annual interest of $1,029. With the average credit card annual percentage rate sitting at 20.48%, it represents an expensive way to fund spending.1,2

Which leads many individuals to ask, “Does it make sense to borrow from my 401(k) to pay off debt or to make a major purchase?”3

Borrowing from Your 401(k)

No Credit Check—If you have trouble getting credit, borrowing from a 401(k) requires no credit check; so as long as your 401(k) permits loans, you should be able to borrow.

More Convenient—Borrowing from your 401(k) usually requires less paperwork and is quicker than the alternative.

Competitive Interest Rates—While the rate you pay depends upon the terms your 401(k) sets out, the rate is typically lower than the rate you will pay on personal loans or through a credit card. Plus, the interest you pay will be to yourself rather than to a finance company.

Disadvantages of 401(k) Loans

Opportunity Cost—The money you borrow will not benefit from the potentially higher returns of your 401(k) investments. Additionally, many people who take loans also stop contributing. This means the further loss of potential earnings and any matching contributions.

Risk of Job Loss—A 401(k) loan not paid is deemed a distribution, subject to income taxes and a 10% penalty tax if you are under age 59½. Generally, should you switch jobs or get laid off, you must repay a plan loan within five years and must make payments at least quarterly.4

Red Flag Alert—Borrowing from retirement savings to fund current expenditures could be a red flag. It may be a sign of overspending. You may save money by paying off your high-interest credit-card balances, but if these balances get run up again, you may have done yourself more harm.

Most financial experts caution against borrowing from your 401(k), but they also concede that a loan may be a more appropriate alternative to an outright distribution if the funds are absolutely needed.

1. NerdWallet.com, 2022 2. TheBalance.com, 2022 3. Distributions from 401(k) plans and most other employer-sponsored retirement plans are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty. Generally, once you reach age 72, you must begin taking required minimum distributions. 4. IRS.gov, 2022

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright FMG Suite.

Lorem ipsum dolor sit amet, consectetur adipisicing elit. Distinctio facilis ea beatae velit qui, temporibus molestias optio vitae libero iure! Lorem ipsum dolor sit amet, consectetur adipisicing elit. Distinctio facilis

Benjamin Franklin once said, “a penny saved is a penny earned.” One way to find the money to meet your spending or saving needs is to examine your current spending habits and consider eliminating money wasters.

Top Money Wasters

Bargain Shopping…and its Expensive Cousin, Impulse Buying: Fire sales and impulse buying (such as products sold on infomercials) can be money wasters, made worse by how often they sit idly in a closet or drawer.

Unused Subscription Services: It can be tempting to sign up for the “free trials” many subscription services offer, but don’t forget to cancel after your trial period is up. Forgotten subscription services can eat away at your wealth when you don’t value the subscription anymore. For example, three $30-per-month subscriptions don’t sound like much until you realize they total nearly $1,100 per year.

Cable and Cell: Call your provider and see if it’s possible to negotiate a new rate. Cell providers, who face stiff competition, may be responsive. Cable companies may be less so, especially if they are a single provider, but you can review your package and make sure you are not paying for service you don’t want.

Paying for Water: Switching from an essentially free product to one that may cost up to $1.50 a day or more is a real budget leak. Consider purchasing a reusable container and using that during the day.

Gourmet Coffee: $4 or $5 a day may not seem like a lot of money, but when Americans step into a gourmet coffee shop, they may often buy more than just the coffee. Consider brewing your own. It can be ready before you leave for work, and it’ll save you the wait in the drive-through line!

Eating Out: While dining out may be one of life’s pleasures, eating out is often less about socialization and more about convenience. Twice a week may not seem like much, but over time it can add up. Try tracking your dining-out expenses for a week. You may be shocked at how fast costs add up.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright FMG Suite.

Understanding the ways credit and debt work for and against you are some of the first steps toward understanding personal finance. While it’s not useful to be scared of credit and debt and avoid it entirely, there are some things to look out for.

Debt

Debt is like any tool: when used correctly, it can be quite useful. When used incorrectly, debt can easily spiral out of control. Missing payments may negatively affect your credit score, and that can take years to recover from. Missed payments, for example, can stay on your credit report for seven years.1

Credit Score

Your credit score is one of the factors lenders use to judge your trustworthiness and qualification for mortgages, auto loans, and other lending. Landlords and employers may also check your credit before renting to you or offering you a job.

Interest

Interest can work against you, but it can work for you, too. When you take out a loan with an interest rate, it’s working against you, but when you invest early and take advantage of compound interest, it’s working for you.

Compound Interest

When you’ve got an account that’s accruing interest, the interest earned gets added to the principal. Then, interest is earned on the new, larger principal, and the cycle repeats. That’s compound interest, baby!

The Value of Time

It’s never too early to start saving. In fact, the earlier you start, the better your result. By getting started with retirement savings sooner rather than later, you can leverage the value of time to your advantage.

Cindy vs. Charlie

Consider the case of Cindy and Charlie, who will each invest a total of $100,000. Cindy starts right away, depositing $10,000 a year at a hypothetical 6% rate of return. After 10 years, Cindy stops making deposits. Charlie, on the other hand, waits 10 years before starting to invest. He also puts $10,000 a year away for 10 years, at the same hypothetical rate as Cindy. After 20 years, who has more money? Shockingly, Cindy’s balance is nearly twice as big as Charlie’s, thanks to the extra time her investment returns had to compound.2

Inflation

Inflation has the potential to eat away the purchasing power of your money. That means, with inflation, the dollar you earn today may not be worth a dollar in the future. Here some things to keep in mind when thinking about inflation.

Cash in a Mattress

Keeping all your cash under a mattress is not only unsafe, it literally costs you money. Assuming the rate of inflation is a hypothetical 2%, every dollar you squirrel away will shrink in value to just $.98 next year.

Rate of Return

Because inflation erodes the purchasing power of your money, any returns you earn on your accounts may not be the “real” rate of return. If your account earned a hypothetical 6% rate of return over the last year, but inflation was 1.5%, your real rate of return was 4.5%.3

Identity theft and safety

In the modern world, identity theft is one of the biggest threats to financial and personal safety. A cracked password or misplaced Social Security number can have big consequences on your current and future finances.

Consider using a password manager

The common wisdom is to use a unique password for each site and service you use. A password manager can make this easier by generating and storing strong passwords until you need to use them.

Sources

Experian, 2020

This is a hypothetical example of mathematical compounding. It’s used for comparison purposes only and is not intended to represent the past or future performance of any investment. Taxes and investment costs were not considered in this example. The results are not a guarantee of performance or specific investment advice. The rate of return on investments will vary over time, particularly for longer-term investments. Investments that offer the potential for high returns also carry a high degree of risk. Actual returns will fluctuate. The types of securities and strategies illustrated may not be suitable for everyone.

This is a hypothetical example used for illustrative purposes only. It is not representative of any specific investment or combination of investments. Past performance does not guarantee future results.

Lorem ipsum dolor sit amet, consectetur adipisicing elit. Distinctio facilis ea beatae velit qui, temporibus

While many people are familiar with the benefits of traditional 401(k) plans, others are not as acquainted with Roth 401(k)s.

Since January 1, 2006, employers have been allowed to offer workers access to Roth 401(k) plans. And some have introduced offerings as part of their retirement programs.1

As the name implies, Roth-401(k) plans combine features of 401(k) plans with those of a Roth IRA.2,3

With a Roth 401(k), contributions are made with after-tax dollars – there is no tax deduction on the front end – but qualifying withdrawals are not subject to income taxes. Any capital appreciation in the Roth 401(k) also is not subject to income taxes.

What to Choose?

For some, the choice between a Roth 401(k) and a traditional 401(k) comes down to determining whether the upfront tax break on the traditional 401(k) is likely to outweigh the back-end benefit of tax-free withdrawals from the Roth 401(k).

Please remember, this article is for informational purposes only and is not a replacement for real-life advice, so make sure to consult your tax professional before adjusting your retirement strategy to include a Roth 401(k).

Often, this isn’t an “all-or-nothing” decision. Many employers allow contributions to be divided between a traditional-401(k) plan and a Roth-401(k) plan – up to overall contribution limits.

Considerations

One subtle but key consideration is that Roth 401(k) plans aren’t subject to income restrictions like Roth IRAs are. This can offer advantages to high-income individuals whose Roth IRA has been limited by these restrictions. (See accompanying table.)

Traditional 401(k)

Roth 401(k)

Roth IRA

Contributions

Contributions are made with pretax dollars

Contributions are made with after-tax dollars

Contributions are made with after-tax dollars

Income Limits

No income limits to participate

No income limits to participate

For 2022, contribution limit is phased out between $204,000 and $214,000 (married, filing jointly), and between $129,000 and $145,000 (single filers)

Maximum Elective Contribution*

Contributions are limited to $20,500 in 2022, ( $27,000 for those over age 50)*

Aggregate contributions are limited to $20,500 in 2022, ($27,000 for those over age 50)*

Contributions are limited to $6,000 for 2022, ($7,000 for those over age 50)

Taxation of Withdrawals

Qualifying withdrawals of contributions and earnings are subject to income taxes

Qualifying withdrawals of contributions and earnings are not subject to income taxes

Qualifying withdrawals of contributions and earnings are not subject to income taxes

Required Distributions

In most cases, distributions must begin no later than age 72

In most cases, distributions must begin no later than age 72

There is no requirement to begin taking distributions while owner is alive

* This is an aggregate limit by individual rather than by plan. The total of an individual’s aggregate contributions to his or her traditional and Roth 401(k) plans cannot exceed the deferral limit – $20,500 in 2022 ($27,000 for those over age 50).

Source: IRS.gov, 2022

Roth-401(k) plans are subject to the same annual contribution limits as regular 401(k) plans – $20,500 for 2022; $27,000 for those over age 50. These are cumulative limits that apply to all accounts with a single employer; for example, an individual couldn’t save $20,500 in a traditional 401(k) and another $20,500 in a Roth 401(k).4

Another factor to consider is that employer matches are made with pretax dollars, just as they are with a traditional 401(k) plan. In a Roth 401(k), however, these matching funds accumulate in a separate account, which will be taxed as ordinary income at withdrawal.

Setting money aside for retirement can be part of a sound personal financial strategy. Deciding whether to use a traditional 401(k) or a Roth 401(k) often involves reviewing a wide range of factors. If you are uncertain about what is the best choice for your situation, you should consider working with a qualified tax or financial professional.

1. To qualify for the tax-free and penalty-free withdrawal of earnings, Roth 401(k) distributions must meet a five-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawal also can be taken under certain other circumstances, such as a result of the owner’s death or disability. Employer matches are pretax and not distributed tax-free during retirement. Once you reach age 72, you must begin taking required minimum distributions. 2. In most circumstances, you must begin taking required minimum distributions from your 401(k) or other defined contribution plan in the year you turn 72. Withdrawals from your 401(k) or other defined contribution plans are taxed as ordinary income, and if taken before age 59½, may be subject to a 10% federal income tax penalty. 3. Roth IRA contributions cannot be made by taxpayers with high incomes. In 2022, the income phaseout limit is $144,000 for single filers, $214,000 for married filing jointly. To qualify for the tax-free and penalty-free withdrawal of earnings, Roth IRA distributions must meet a five-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawal also can be taken under certain other circumstances, such as a result of the owner’s death or disability. The original Roth IRA owner is not required to take minimum annual withdrawals. 4. IRS.gov 2022

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Chris Muha

Managing Director of Corporate Benefits

Chris is the Managing Director for Corporate Benefits at Capstone. Chris is primarily focused on client engagement, retention and building out strategic partnerships for the firm. As an expert in the employee benefits industry, Chris brings more than a decade worth of experience. Prior to joining Capstone, he worked for NFP on their Business Development Team as a Senior Advisor.

He is a graduate of The Catholic University of America, and currently resides in Washington, D.C with his wife Caitlyn, and their two sons Jack and William. In his free time, whenever he has it, he enjoys his Peloton, Running and Golf.

Josh Monk, MBA

Director of Wealth Management

Joshua Monk joined Capstone Retirement Group in 2015 as Director of Wealth Management. He also serves as a Senior Financial Advisor, Portfolio Manager, and Education Specialist. he earned is Master’s Degree in Business Administration and Finance from Oklahoma City University in 2006. Since that time, Josh has worked in the financial services industry as a Financial Advisor in Private Wealth Management and a Consultant to Financial Advisors on an institutional level.

Prior to joining Capstone Retirement Group, Josh served as a Financial Advisor at Merrill Lynch and SunTrust Investment Services, inc., as well as a consultant to elite Financial Advisors while at ProShares Advisors, LC. his duties included financial planning, investment management and business banking.

At Capstone, Josh specializes in guiding individuals through the financial planning process by designing a holistic financial strategy and offering tailored investment solutions for the individuals and their families. His approach will consider your risk tolerance, time horizon, liquidity needs, and overall investment goals.

Josh holds a FINRA Series 7 (General Securities Representative) and Series 66 (Uniform Combined State Law Examination). He also holds Life, Health and Variable insurance licenses in VA, MD, & DC.

Josh resides in Washington, DC with his wife Cassie, and two sons. As a graduate of the University of Oklahoma in 2004, he is an avid fan of the Oklahoma Sooners.

Richard Banziger

Founder/Managing Director,

Retirement Services

Richard is the President and founding member of the Capstone Retirement Group. He manages the group’s strategic client relationships and develops growth opportunities for the practice. Richard also serves as the key liaison between Plan Sponsors and Plan Service Providers, ensuring a high quality of standards and service for clients. He is an expert in plan design, participant education, fiduciary oversight, investment selection and service provider management.

Richard brings more than 30 years of qualified retirement plan experience and holds various securities licenses.

Richard is a graduate of James Madison University and currently resides in McLean, VA.

Taylor Wall, CRPS®

Director of Client Services

Taylor Wall serves as Director of Client Services for the Capstone Retirement Group. Taylor pro-actively supports new and existing client relationships. He assists in providing ongoing investment analysis due diligence, fiduciary oversight support, and assistance to plan sponsors, including administrative investment option plan change processing and reconciliation.

Taylor is licensed and credentialed as a Chartered Retirement Plan Specialist.

Taylor resides in Alexandria, VA. In his free time, he enjoys playing golf and watching college and professional sports.